Personal finance doesn't always have to be personal. Sometimes it's shared — like when you open a joint bank account with a partner, family member, or roommate.

Whether you're splitting rent, saving for a shared goal, or looking for an easier way to manage household expenses, a joint bank account could simplify things. Here's everything you need to know: what joint accounts are, how they work, their advantages and disadvantages, and how to decide if one is right for you.

What is a joint bank account?

A joint bank account is a chequing or savings account shared by two or more people, where every account holder has equal access to the funds and equal responsibility for the account. It works the same as an individual account — you can make deposits, withdrawals, bill payments, e-transfers, and other transactions — the difference is that more than one person can do all of those things.

With shared access comes shared responsibility. If one account holder overdraws the account, for example, the resulting fees are the responsibility of all parties on the account.

Who can open a joint bank account?

Joint bank accounts go beyond couples who want to combine finances. Roommates could open a joint account to pay for shared living costs. Co-founders might need multiple joint accounts to manage business expenses and save for future expenditures. Parents often open joint accounts with children to help manage their savings and give them access to spending money (after their rooms are clean, of course).

How to open a joint bank account

Opening a joint bank account is straightforward. In most cases, all account holders need to visit a branch together or apply online, depending on the financial institution.

Here's what you'll typically need:

Valid identification — each account holder needs government-issued photo ID (such as a driver's licence or passport)

Social insurance numbers — your bank needs these for tax reporting

Proof of address — a utility bill or bank statement showing your current address

Agreement on account type — decide whether you want a joint chequing account, savings account, or both

Before you sign anything, make sure you understand the account agreement. Ask your financial institution about their policies on joint accounts — specifically, whether all account holders need to authorize withdrawals or one signature is sufficient.

Advantages of a joint bank account

Shared expenses are simpler. There's no need to transfer your half of the rent or dinner bill when it's all coming out of one account.

Saving for common goals is easier. By saving up for a vacation or new furniture in a shared account, you can watch together as your individual deposits join forces and get you to your target faster.

More transparency and accountability. Joint accounts give everyone a clear view of what's coming in and going out. That visibility can boost accountability when it comes to spending and saving, making it easier to create and follow budgets and other financial plans.

Disadvantages of a joint bank account

Shared liability. Both account holders are on the hook for debts and fees incurred by the account, whether or not one person is to blame. In a serious financial or legal situation, creditors could seize the shared funds in the account.

Less control over the money. With many joint accounts, one account holder can't control the actions of another. Each person can withdraw however much they want, whenever they want, without penalty. That's why you should open a joint account with someone you genuinely trust.

No financial privacy. There's nowhere to hide in a joint account. If one of you isn't contributing equally — or suddenly decided to pay for stand-up paddleboarding lessons from your emergency fund — you're probably in store for some arguments.

Tips for managing a joint bank account

A joint account works smoothly when everyone's on the same page. Here are a few ways to keep it that way:

Agree on the account's purpose upfront. Decide together what the account will be used for (rent, groceries, savings) and what it won't.

Contribute proportionally. If one person earns more, consider contributing a percentage of income rather than a fixed amount so it feels fair to both.

Set a spending threshold. Agree on a dollar amount above which you'll check in with each other before spending.

Review the account regularly. Monthly check-ins help you stay aligned on spending and savings goals.

Keep individual accounts too. Maintaining your own account alongside the joint one gives you financial autonomy and a safety net.

Joint accounts and legal considerations

Joint accounts and debt

If one account holder has outstanding debts, creditors may be able to access funds in the joint account to settle those debts — regardless of who contributed most of the money. Before opening a joint account, it's worth having an honest conversation about each person's financial situation.

Joint accounts and relationship breakdown

In a separation or divorce, the law in your province may treat a joint account as a shared asset. Depending on the province, a court could divide the funds as part of the settlement. If a relationship ends, either account holder can typically withdraw funds at any time — which is why trust is so important from the start.

What happens to a joint account when someone passes away

In most provinces, joint bank accounts include a right of survivorship. That means when one account holder passes away, the remaining funds automatically transfer to the surviving account holder — without going through the estate. However, the rules vary by province, and the account agreement matters. It's a good idea to confirm your financial institution's policy and consider how joint accounts fit into your broader estate plan.

Single account vs. joint account: which is right for you?

Whether a single account or a joint account is the right fit for you depends on how you plan to use the account, as well as your individual habits and preferences.

Remember: these two accounts are not mutually exclusive. You can — and sometimes should — have both a single account and a joint account.

When a single account makes sense

You want to maintain a sense of financial autonomy.

You don't want someone else to have a full view of your transactions.

You have personal savings goals.

The other person carries significant debt, and creditors could hold you responsible for it.

When a joint account makes sense

You have many regular shared expenses and bills.

You need transparency in order to create and manage a joint budget.

You're saving as a team for a shared purchase.

You want to build a household emergency fund.

You want an oblivious friend to help pay for your stand-up paddleboarding lessons (kidding!).

Making the most of your joint account

A joint bank account isn't a commitment you should take lightly — but with the right person and a little planning, it can make managing shared finances significantly easier. The key is clear communication: agree on what the account is for and revisit the arrangement as your circumstances change.

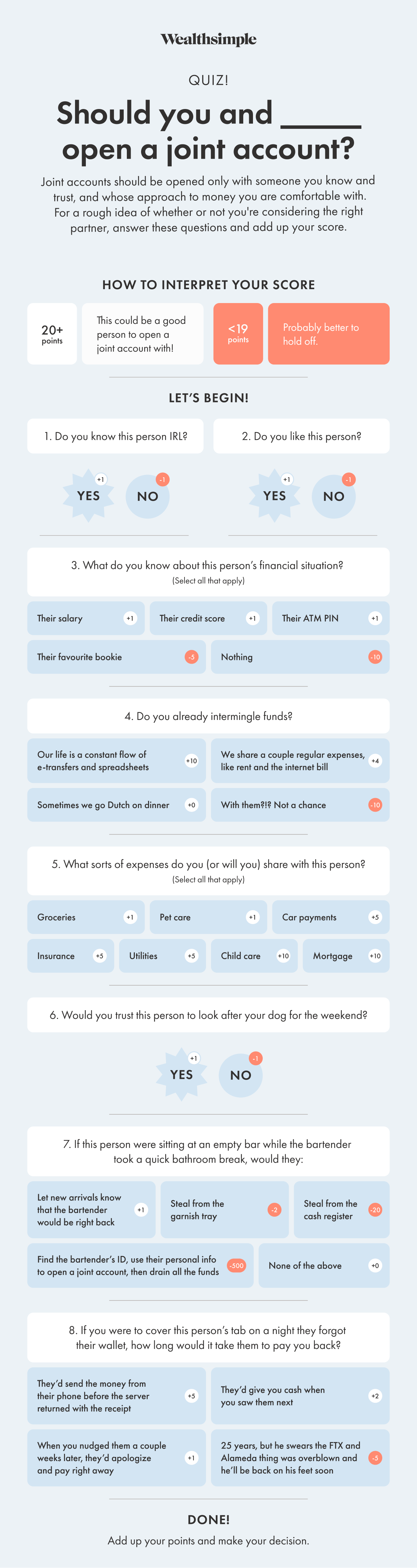

Bonus Quiz! Is this the right person to open a joint account with?