Isn’t a chequing account the same thing as a savings account, only you have more access to your money? Is one better than the other? Do you really need two accounts? What’s the point?

A chequing account is a “transactional” account or an account where the bank expects the account holder to make frequent transactions with the money deposited in that account. Transactions include depositing and withdrawing cash, using your debit card to pay for things, and having money electronically wired into your account.

There are chequing accounts available to students (usually with no fees attached), corporate accounts used by businesses, or joint accounts, usually used by married couples.

Unless otherwise determined by the bank, chequing accounts usually have some type of fee associated with them. Fees can be charged when you use an ATM, when you use your debit card abroad, or when you overdraw your account. Sometimes checking accounts hit you with a combination of all those fees (boo).

A savings account, on the other hand, is not really meant for transactions. It's used as an “emergency” checking account all the time, of course, but its purpose is to provide a safe place to store your money long-term. Michael Craig, advisor at Wealthsimple, explains one of the reasons you should have a savings account.

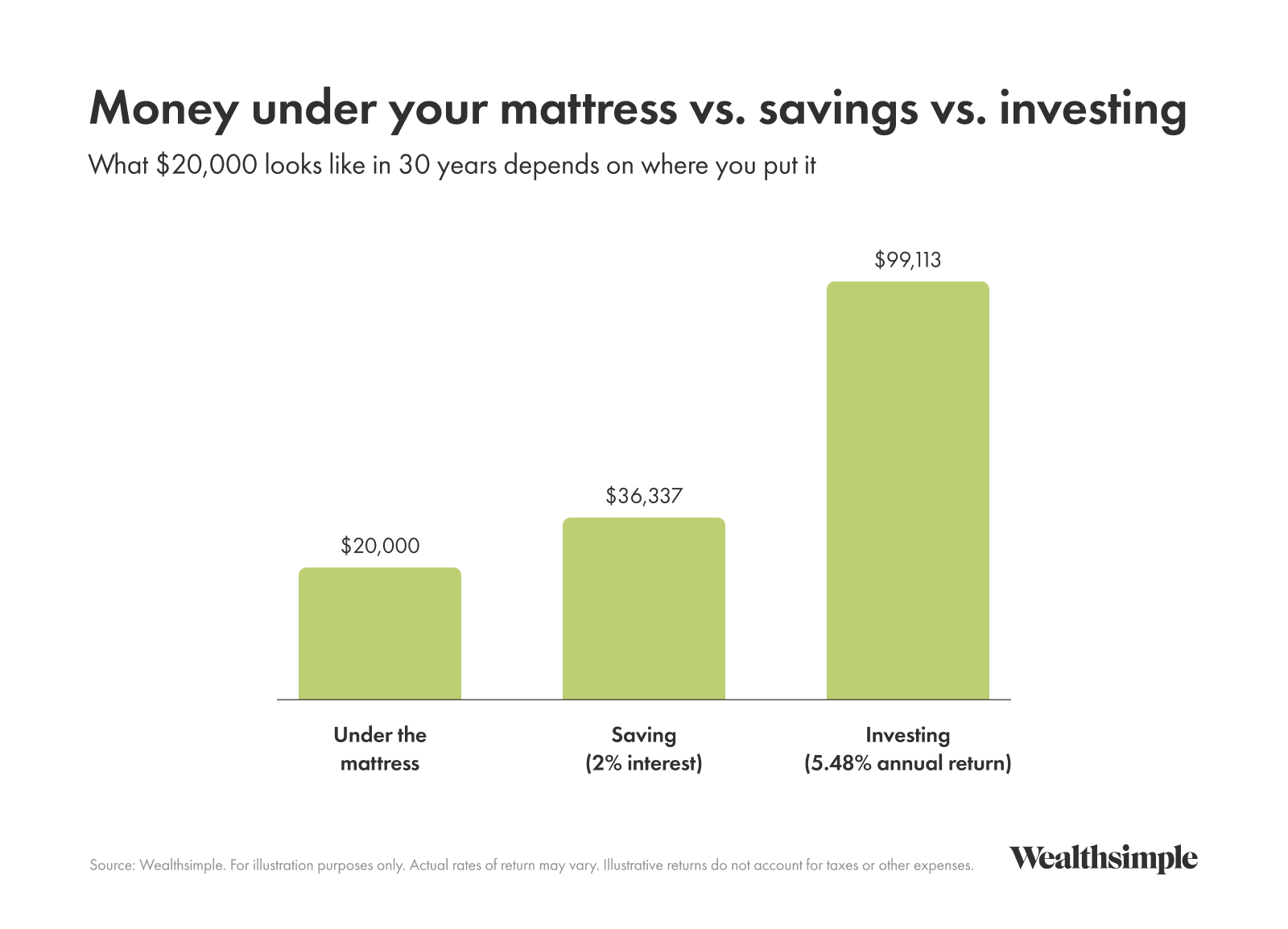

Since the money in a savings account is used by banks to make loans to other people, the bank will pay you interest on your balance. Returns probably aren't going to be as high as those you’d receive if you were to start investing. But it's the stability of savings accounts that make them such a worthwhile financial tool. Any interest earned is a kind of bonus.

You might be wondering why you’d even bother with a savings account if you could just invest your money into a low-fee diversified portfolio. But a savings account is a foundation. It supports other types of investing, allowing you to keep a certain amount of funds safe and sound, unaffected by the ups and downs of markets.

While the money in a savings account is harder to access than money in a chequing account, a savings account still has more liquidity than the money you invest. Plus, you get (modest) returns without any of the risks associated with investing your money. Should you ever need money immediately, it's there and can be withdrawn or transferred to your chequing account without penalties.

You can open a tax-free savings account (TFSA) and benefit from all the tax breaks that come with it. The word “saving” might be a little confusing because you can actually use these accounts to save or invest. As the name suggests, the major advantage of these accounts is that interest earned is tax-free.

Pros and cons

The differences between a chequing and a savings account boil down to accessibility, fees, and interests.

Pros and cons of chequing account

Pro: Offers high accessibility through debit cards, ATMs, checks, and mobile banking

Con: Usually has fees

Con: The money you put in a chequing account will not accumulate interest and lends itself badly to saving since you’re always using your checking account for things like groceries, late-night impulse buys, or your Saturday night bar tab. So yeah, not the best account for trying to save up for a mortgage payment.

Pros and cons of a savings account

Pro: Generally, savings accounts have few to no fees (but check the fine print; some banks require you to have a minimum balance in your account or make frequent deposits)

Pro: Offers interest on your money (rates can vary wildly, so check)

Pro: Offers tax-free returns if you’re signed up for a TFSA

Con: Isn’t designed for frequent withdrawals. Some banks will often limit the amount and frequency of the withdrawals you can make.

When to use a savings account over a chequing account

At the end of the day, it comes down to your financial goals and habits. As mentioned above, it’s best to think of a chequing account as an everyday kind of deal: You use it to pay for your morning coffee, drinks with coworkers, IKEA runs, and everything else that makes up the tapestry of your daily life.

You should be using a savings account for something you’re aiming to pay (or pay off) within three years — whether that be a vacation, a down payment on a house, or for paying taxes you know you’ll owe. A savings account is also a great place to put your emergency fund — money you’ll want on hand in case of job loss or any other unforeseen expenses. As a rule, it’s recommended for you to have between three to six month’s worth of expenses saved up in your emergency fund.