You can save money in all sorts of ways. You can put cash in a safe. You can simply mentally categorize a certain amount of money in your checking account as “savings.” But it’s crucial to put savings in an account created specifically for that purpose. It’s safest there, it's a good place for an emergency fund and provides you with the ability to buy something expensive. Plus it’s earning a little interest.

You can open a traditional savings account at your bank. Or you can open a hybrid type of account which is kind of like a chequing and savings account combined.

That all sounds kind of… boring, right? And, you know what, it is kind of boring. But in personal finance, the boring stuff allows you to do exciting stuff like achieving financial freedom and not having to work any more as Michael Tempelmeyer, advisor at Wealthsimple explains.

What saving a little money and keeping it handy allows you to do in the long term—like have more fun and, you know, provide for your family—isn’t boring at all. Now that you know where to start, here's how to get some money from your pocket into that savings account.

How to Save Money

Now that you know the best way to start saving money — how do you actually go about doing it? There are a number of tactics that will help you stop spending and start saving.

1. Set a budget. It’s hard to know how much you’ll be able to put away in savings if you don’t know how much money you’ll… be able to put away in savings. Putting away too much too early can wreak havoc on your chequing account and might require you to transfer money back into your chequing and create a strain on your finances generally.

2. Automate your savings. Most financial institutions allow you to link your chequing account with your savings account so that a certain amount of money will move into savings without you having to even press a button. Many employers will allow you to split your direct deposit so that part of your cheque goes straight into savings. Even if they don't, try to have the auto-deposit happen on payday and you'll hardly miss the money you would have otherwise spent.

3. Cut down on eating out and trips to the coffee shop. Could you get by on two cups of coffee, not three… or eight? Or one lunch out each week rather than four or five. Starbucks is expensive and so is eating out. If you're willing to start brewing your own coffee and channeling your inner Gordon Ramsay, you stand to make a ton of savings. When you do go out try to hold yourself back from ordering the most expensive item on the menu or ordering lots of alcoholic beverages that have a high markup.

4. Take advantage of anything that's free. They say the best things in life are free. And you should absolutely avail of them. Look up free events in your local area. Take trips to local parks and beaches. Go and visit your museum on days it's free. Take advantage of free subscription services like Spotify, visit your local library rather than buy books or join clubs that often hold free events.

5. Save your spare change. In the last few years, a handful of apps have been created to automatically take small increments of money and deposit them in an investment or savings account. These services redirect funds that you would never know are gone. (This speaks to a certain rule of saving: Save small but save a lot. “Small” can mean different things. More on that in a bit.) Some direct a certain percentage of your paycheque to savings. Some will even help you find subscriptions that you may have forgotten about so you can cancel them and allow the app to allocate that money toward savings.

6. Use public transport. Now might be a good time to stop ride-ordering your potential savings away and start taking public transport. Better yet, walk, or cycle. All those $10 trips add up to a lot over the course of a month and even more over a year, not to mention the costs involved in owning a car. There might be some occasions when taking a taxi is an absolute must but when you can — use public transport or walk to save on transport costs.

7. Take advantage of employer retirement contributions. If you work for a company that matches your retirement contributions — you should absolutely take them up on this offer. You're essentially getting “free money” and in most cases doubling the amount you're saving. If you have a couple of pension plans lying around, you could save money by transferring them to a low fee investment provider.

8. Reduce fees charged by your bank. Bank fees might seem small, but they all add up. Banks have a way of slapping on fees each time you do anything, from using an ATM that's not theirs to not keeping your savings account balance above a certain level. Be aware of the fees your bank charges and try to avoid them. Only use their ATMs and consider opening or moving your savings account or savings investment account to a provider that requires no account minimum balance or transfer fees. Your wallet will thank you for it!

9. Save your tax refund. If you have been lucky enough to get some taxes back from the government — save them rather than spend them. You can absolutely do without this money, you've hardly missed it over the course of the year, you won't miss it now. This is a quick way to save a large sum of money.

10. Travel during off-peak season. We don't blame you if you're a fan of jet-setting. And we're not saying don't do it — but rather look at how you can reduce the cost of your vacation. Set up price alerts on flights, book well in advance and travel during the off-peak season. Remember, peak season in some countries might be different from that of your own.

11. Do house swaps or rent an apartment over a hotel. When traveling, staying in hotels can rack up a pretty penny. Particularly if you are travelling with a family. Instead, consider doing a house swap. This still allows you to make the trips you always wanted to while saving money at the same time. If you're not in a position to do a house swap, consider renting an apartment or a room in a house on Airbnb or another apartment rental service.

12. Cancel subscriptions (or find cheaper versions). Chances are, you have a few subscription services that you've forgotten you ever even signed up for. Now would be a good time to cancel those. Do some digging in your bank or email account to figure out how much they are costing you. Decide which to keep and which to cut or at very least try and find a cheaper alternative.

13. Do things yourself. While it will take you some extra time, doing things yourself rather than having someone else do them is a great way to save money. Using a laundry service or hiring a handyman can be costly over the course of a year. So get off the sofa, head to the store, buy some laundry detergent and maybe a hammer and start saving the money you would have otherwise given to other people.

14. Submit your expenses (if your work entitles you to). If you work at a company that allows you to expense travel, food or other costs you incur — make sure you don't forget to claim them. This is money you have effectively loaned your company and getting it back is as easy as submitting a few receipts. If you’re not an avid receipt hoarder, use your phone to take pictures of them. That way, you'll never lose them.

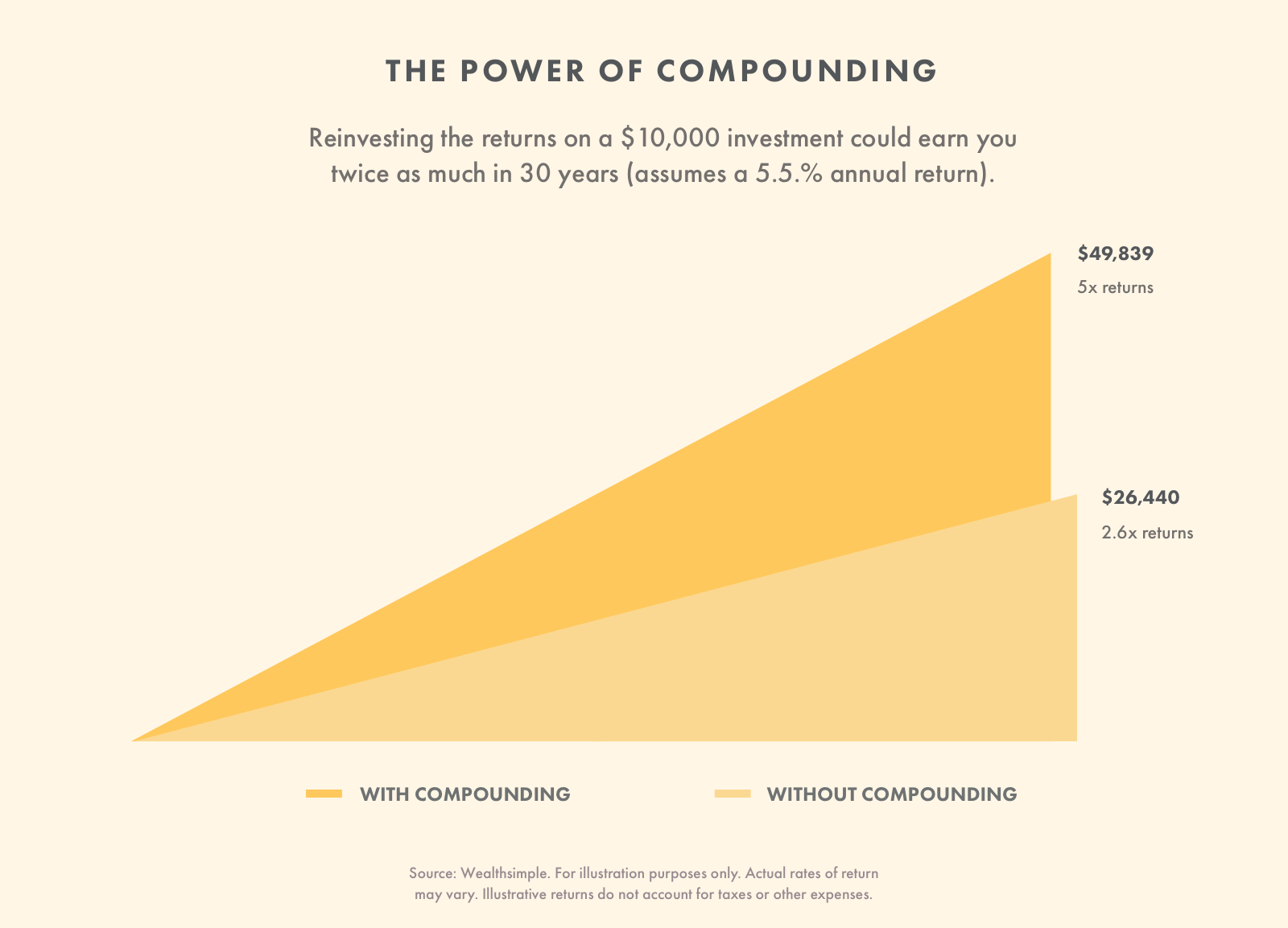

15. Start investing. The sooner you start investing the sooner you start benefiting from the power of compounding. This essentially means — giving your money more time to make money. If you're saving for something far into the future like retirement or a young child's education, you might be better off investing opposed to saving. In the past, inflation outpaced savings account interest rates. Investing typically (but not always) provides higher returns, which also sometimes means taking higher risk, provided you can lock your money away for a long period of time.

16. Move away from buying branded items. Do you have to buy Gucci shoes or Ralph Lauren shirts...probably not? We're all for doing things that make you happy — even if that means buying a few designer items. But if your designer wardrobe is the culprit of your lack of savings, it's time to reevaluate your shopping habits. We're not saying buy cheap clothing that's not going to last a single wash but rather seek out good quality clothing that doesn't cost the earth.

17. Stop buying bottled water (if you don't have to). Bottled water can be expensive. If drinking tap water is safe in your area, there's little reason to buy bottled water. Consider swapping to a water jug with a filter or a reusable water bottle. There are water fountains in most public places from shopping malls to airports — so there are no excuses! Not only is this kind to the environment, but it will also be kinder to your pocket.

18. Avail of reward programs. There is a reward program for almost every day of the month and signing up for rewards or rebates could end up saving you a lot. If your local grocery store gives back 5% on a rewards program and you spend $100 a week there — that's an additional $20 a month that you otherwise would not have had. Sign up to a couple of reward programs like this and it can amount to quite the sum of money.

19. Use promo codes online or collect coupons. Believe it or not, but some of the wealthiest people in the world collect coupons. And with good reason — you stand to save a lot. The modern version of coupon collecting is searching for promo codes online when you shop.

20. Compare gas and car insurance prices (if you have a car). Shop around to save money on gas as the price varies from place to place. Look out for gas station rewards cards as many have loyalty programs that can save you money over the long run. When buying a new car, make sure it’s fuel-efficient. Even if the car is more expensive than other inefficient models you could end up saving more in the long run. It can also pay to shop around for the cheapest car insurance rather than accept the quote your current insurance company provides each year.

21. Use a credit card with a good FX rate or rewards. If you travel internationally or spend money in another currency, Peter Keung, founder of HighInterestSavings.ca, recommends taking out a credit card that waives the foreign currency exchange fee. Peter explains the fees on currency conversion are often in the region of 2.50%. If you don't spend money in other currencies you could find a card that offers rewards or points when you spend money. That said, Peter explains these credit card rewards only make sense if you live within your means and don't overspend on your credit card.

Keung recommends using cash or a debit card if you have a tendency to get carried away with your spending. When you use a debit card, you feel the immediate hit on your bank account and it's hard to spend more than you can afford.

Now that we’ve gone through some tactics to help you save, let’s drill down on a few quick and easy ways to save money.

Saving money in Canada

There are savings tools available in Canada that you might not consider “savings” tools at all. Consider an RRSP account. It’s a retirement investment account, right? But its goal is to help you save for retirement. The money in an RRSP can be used to buy investments like mutual funds, ETFs, stocks, and bonds, but you don’t have to pay any tax on any interest, dividends, or capital gains you earn until you take them out. For example: If you made $60,000 and you contributed $5,000 to your RRSP, you will pay tax on only $55,000 of income. (That’s a lot of savings!) When you do have to pay taxes when you retire, you’ll enjoy a much lower tax bracket.

An RESP works in a similar way, only it’s specifically meant for your child’s education. Then there’s a Tax-Free Savings Account (TFSA), which works much the same way as an RRSP, only your money is available to you any time you want it. These are savings tools that almost every financial advisor wants you to take advantage, and with good reason. If you have not been availing of the tax breaks from accounts like these — they are absolutely a great place for you to start saving.

Easy ways to save money

We've covered a ton of tactics you can use to save money — but all these tactics might not be for you. Here are some easy ways to save money that will apply to almost anyone.

Minimize your spending

The easiest way to save money is to continue making the same number of purchases you do now only minimizing each purchase. This won’t grow your account very quickly, but it will allow you to sock money away dozens of times each week. Start by looking at the things that cost you the most money. Cutting a few large expenses has the potential to save you a lot of money. You still get to do all the things you love, but you also save money.

Examine all recurring bills

Look at your recurring bills including telephone, insurance, cable, gas, and electricity. What if you got on the phone with your service providers and asked if you could get a better rate? Called your cable company and asked if you could bundle your internet and phone together? Called your insurance agent and asked if you could get a better rate? (Insurance agents always seem to be able to get people better rate. Just give us a good rate, insurance agents!) What’s the worst that could happen? They say no? (They probably won’t say no.)

These phone calls will result in way more than one-time savings. They’ll pay off for years to come. If you knock $15 off your phone bill, in five years you’ll have another $900 or so in savings. Do that with five other bills and you’re looking at almost $5,000. All for the price of a few phone calls.

Don't buy things you already own

Another easy way to save money: Don’t buy things you already own. Do you really need to replace that set of dishes? Is that stain on the sofa really that noticeable? (It’s a charcoal sofa! That’s what charcoal was created for — so everything can be stained. Is it really that big of a deal that there’s a song that skips on disc 3, side 2 of your otherwise pristine vinyl box set Grateful Dead: Cornell 5/8/77? … Oh, the song is “Fire on the Mountain”? Yeah, you should absolutely replace that. Otherwise, put the money you would’ve spent on those things right into savings.

How to save money fast

So you're looking to save money for a holiday in the Bahamas, a house, wedding, new car or anything else fun. You don't have years to wait, you need to do it fast — here's how.

Zoom Out

Saving fast (ironically) requires you to pause and look at your monthly purchases all at one time. You need to zoom out. Any list of purchases will do. Look at your chequing account statement. Look at your grocery receipt. Look at that handwritten bill of sale from the general store (19th-century readers only). The point is: Get a big-picture sense of how you spend your money so you can start immediately changing your money-saving habits.

Identify Recurring Expenses

Find recurring expenses that aren’t regular, automatic subscriptions. If you look at those purchases, you’ll start seeing patterns in your spending and those patterns will reveal lots of ways to save money, starting right now. (Also: Congratulations, you’re a financial analyst!)

Take food, for instance. Food takes up more of your disposable income than you’d think. Most people spend around 10% of their income on food. That expensive hemp milk you threw in your cart on aisle 12 may have seemed like a fun purchase in the store, but staring back at you in black and white on a receipt in between the cashew milk and flax milk you also bought (wow, you’re really into non-traditional milk!)… Well, it just seems frivolous.

Look for similar kinds of purchases. There will be lots of them. Start winnowing those down to a list of purchases each that provided real entertainment and value to your life. Buy what you really love. Steer clear of forgetful purchases.

Save on grocery shopping

For grocery shopping in particular, make a list and stick to it, don't visit the most expensive store, buy in bulk, purchase fruit and vegetables that are in season (they're cheaper) and swap from branded to unbranded products provided the quality is similar.

You’ll find that the habit of buying only the things you need or truly value will begin changing other habits. Like your caffeine intake or your habit of buying and restoring personal jetpacks. Cool hobby! But the money you’re spending on it will better serve your financial future. And if it’s something you are constantly spending money on, the results will be relatively instantaneous.

How to save money fast

So you're looking to save money for a holiday in the Bahamas, a house, wedding, new car or anything else fun. You don't have years to wait, you need to it fast — here's how.

Zoom Out

Saving fast (ironically) requires you to pause and look at your monthly purchases all at one time. You need to zoom out. Any list of purchases will do. Look at your checking account statement. Look at your grocery receipt. Look at that handwritten bill of sale from the general store (19th-century readers only). The point is: Get a big-picture sense of how you spend your money so you can start immediately changing your money-saving habits.

Identify Recurring Expenses

Find recurring expenses that aren’t regular, automatic subscriptions. If you look at those purchases, you’ll start seeing patterns in your spending and those patterns will reveal lots of ways to save money, starting right now. (Also: Congratulations, you’re a financial analyst!)

Take food, for instance. Food takes up more of your disposable income than you’d think. Most people spend around 10% of their income on food. That expensive hemp milk you threw in your cart on aisle 12 may have seemed like a fun purchase in the store, but staring back at you in black and white on a receipt in between the cashew milk and flax milk you also bought (wow, you’re really into non-traditional milk!)… Well, it just seems frivolous.

Look for similar kinds of purchases. There will be lots of them. Start winnowing those down to a list of purchases each that provided real entertainment and value to your life. Buy what you really love. Steer clear of forgetful purchases.

Save on grocery shopping

For grocery shopping in particular, make a list and stick to it, don't visit the most expensive store, buy in bulk, purchase fruit and vegetables that are in season (they're cheaper) and swap from branded to unbranded products provided the quality is similar.

You’ll find that the habit of buying only the things you need or truly value will begin changing other habits. Like your caffeine intake or your habit of buying and restoring personal jetpacks. Cool hobby! But the money you’re spending on it will better serve your financial future. And if it’s something you are constantly spending money on, the results will be relatively instantaneous.

Ways to save money on a tight budget

Saving on a tight budget can seem counterintuitive. If you’re already struggling to pay your bills, how do you set any meaningful amount away in savings?

The key is looking at every amount—no matter how small—as meaningful. If the reason money is tight is that you’ve maxed out your credit cards, then work on paying down your debts. A big credit card balance can be a drain on your financial situation for years and years. Savings aren't really savings when you have a fat credit card balance. It’s just money that you’re not allocating to your credit card balance.

What’s true for tight budgets is true for any budget. Any of the above tips will work for tight budgets. Notice that there’s no dollar amount attached to any of the advice in this article. Fifty cents matters. A dollar matters. Ten dollars matters. The goal is not to infuse your account with money. The goal is to work toward the goal itself. Every day. You’ll see your account tick up, which will motivate you to save even more.

Top tips for saving money

There's a trick to being a good saver, not just for a week or month but forever. It consists of making lifestyle changes, creating good savings habits and following some rules. Here are our top saving tips to help you become a great saver for life.

Get into the habit of saving

Our top tip is to get into the habit of saving. Cut your costs, look for ways you can make more money and put away some money for savings each month — even if it’s a small amount.

Successful saving is a habit. Once you start in on it, it will become second nature. You’ll see two products in the store, one two dollars more than the other, and you’ll imagine that $2 difference floating into your savings account. Congrats, you just provided yourself with financial security.

In many ways, saving money is about what you don’t choose. It’s almost passive. It’s about doing a stay-cation so you can go on a better vacation later. Thankfully, though, there are products available that allow you to not do anything at all. Or even think about saving.

Even when you consider long-term big-picture savings accounts like retirement savings, you’re still incrementally building up an account and providing for your future needs. You’re thinking small but making something big.

Follow the savings plan formula

You may or may not have heard of the 50:30:20 rule. If not, it's essentially a master plan for your finances. This rule states that you should spend about 50% of your income on needs like your rent or mortgage payment and your health insurance. You should spend no more than 30% on wants like designer shoes or vacations and the other 20% should be saved or invested. This is an easy rule that does not involve any complicated calculations — but rather some simple math.

Those looking not just to save but create a game plan for their overall finances would do well to consider creating a savings plan. A formula like the 50:30:20 one is a great starting point.

Avoid lifestyle creep

It's likely that you'll make more money in your thirties than you did in your twenties and more in your forties than in your thirties and so on. One clever way to save money, almost without realizing it — is to avoid “lifestyle creep” at all costs. Lifestyle creep means that as soon as you start earning more money, you instantly upgrade your life. Think — getting a better apartment, nicer clothes, a more expensive car or a nice watch. Suddenly all these luxury items become necessities and you've thrown a ton of money that could be saved, right down the swanny. When you get a raise, a bonus, inheritance or an influx of money — as tempting as it might be to spend, save the money instead.